Endorsements

To add your organization to the list please email info@DarnAir.org.

- Brighton Resort

- Capitol Hill Action Group (CHAG) in SLC

- Conserve Southwest Utah (CSU)

- Fridays for Future Utah

- Great Old Broads for Wilderness

- IME Utah (International Mountain Equipment, climbing gear)

- League of Women Voters, Utah and SLC chapters

- Mormon Environmental Stewardship Alliance (MESA)

- Taxpayer Association of Kane County

- The Front Climbing Club (2 locations in SLC, 1 in Ogden)

- Utah Citizens’ Counsel

- Western Wildlife Conservancy

One-Paragraph Summary

This material is archived from our 2020 campaign; see the blog for updates for 2024.

The carbon tax starts at $12 per metric ton CO2 (about 11 cents per gallon of gasoline, about 1 cent per kWh of electricity) in 2022; there is a reduced rate for agriculture, mining, manufacturing, and other energy-intensive trade-exposed businesses to help them stay competitive. The tax goes up slowly over time and funds:

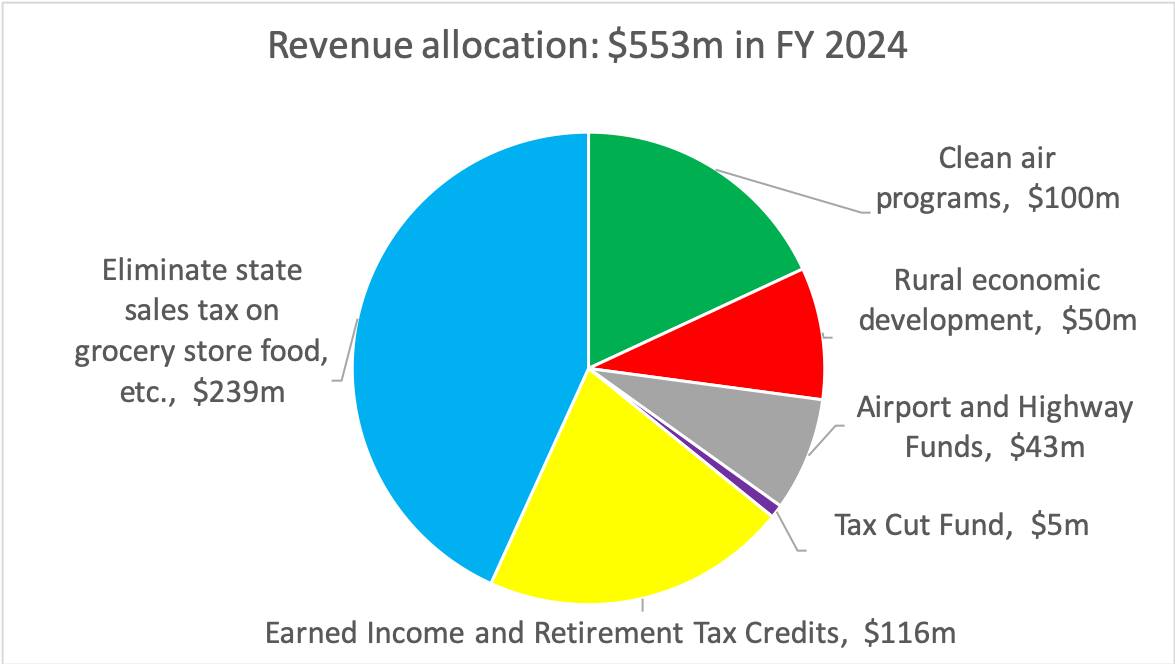

- $100 million a year for cleaning up local air pollution from wood-burning stoves, gas-powered lawnmowers, freight-switcher locomotives, dirty school buses, and more.

- $50 million a year for rural economic development.

- Elimination of the state sales tax on grocery store food and other regressive sales taxes.

- A 20% match of the federal Earned Income Tax Credit for low-income working families.

- An expansion and extension of the Retirement Tax Credit.

- Additional tax cuts if possible, as determined by the state legislature.

Pie chart source: This pie chart is based on the final Fiscal Estimate spreadsheet for our measure.

One-Page Summary

This material is archived from our 2020 campaign; see the blog for updates for 2024.

The carbon tax starts at $12 per metric ton CO2 in 2022 and goes up at 3.5% plus inflation, reaching (in real terms) $15 per ton in 2029, $20 per ton in 2037, etc., up to a maximum of $100 per ton. It applies to motor fuels ($12 per ton is ≈11 cents per gallon), electricity consumption (≈1 cent per kWh, but it depends on each utility’s fuel mix), and natural gas (≈6 cents per therm); for all of these, $12 per ton CO2 is at or below 10% of current retail prices. The tax also applies to coal, off-road diesel, and fuel gas used by large facilities—such as refineries and steel mills, but not power plants because the electricity tax is on consumption—that emit over 10,000 tons of CO2 per year (equivalent to about 1 million gallons of diesel).

To help them stay competitive in national and international markets, industrial users (e.g., agriculture, mining, and manufacturing companies) get a reduced rate: 10% of the standard rate in year 1, 15% in year 2, etc., and then 50% in the second decade and beyond. Off-road diesel is only subject to the carbon tax in facilities that emit over 10,000 tons of CO2 per year.

Most of the revenue from the carbon tax would go into a Carbon Emissions Fund, except that federal regulations essentially require taxes on jet fuel to go into an Airport Fund. (Also, as required by Utah’s constitution, the carbon tax on motor fuels goes into the Highway Fund, but a roughly equivalent amount of the sales tax money currently going to highways is put into the Carbon Emissions Fund instead, the net impact on the Highway Fund being slightly positive.)

This Carbon Emissions Fund revenue is directed as follow, in order of priority:

- Transfers to the Education Fund to make up the lost revenue from the 20% match of the federal Earned Income Tax Credit and from supplementing the Retirement Tax Credit (which is expanded from a maximum of $450 per person to $650 per person, with eligibility extended by 10 years, from born-before-1953 to born-before-1963).

- Transfers to the General Fund to make up the lost revenue from eliminating the state sales tax on grocery store food (and also eliminating the state sales tax on electricity and heating fuels, which will partially cushion the price impact of the carbon tax while still giving electric utilities an incentive to reduce emissions).

- Annual spending of $100m on improving air quality ($25m to the CARROT program, which reduces emissions from school buses, industrial vehicles, and lawn equipment, and $75m to DEQ for a Clean Air Grants Program) and $50m on rural economic development through the Governor’s Office of Economic Development. The $25m for the CARROT program (Clean Air Retrofit and Replacement of Off-road Technology) gets top priority, then the $50m for rural economic development, and then the $75m for the Clean Air Grants, which goes away if and when the state meets Clean Air Act standards.

Any remaining revenue goes into a Carbon Emissions Tax Refund Restricted Account that the legislature can only use to “lower state taxes, especially for low- and middle-income households and for energy-intensive trade-exposed businesses.”

All the Legal Details

This material is archived from our 2020 campaign; see the blog for updates for 2024.

Here is our final legal language and our final Fiscal Estimate, both also available from the Lt Governor’s website. Read on for a technical overview, and a section-by-section description that covers all the sections, which in order are 19-1-207 and 19-1-208 (certification of large emitters and electricity providers); 19-2-401 (Clean Air Grant Program); 35A-8-308 and 35A-8-309 (sales tax administrative changes); 59-10-1019 (Retirement Tax Credit); 59-10-1102.1 and 59-10-1113 (Earned Income Tax Credit match for low-income working families); 59-12-103 (sales tax changes); 59-30-101, 59-30-102, and 59-30-103, 59-30-104 (carbon tax title, definitions, records, and amended returns for large emitters and electricity providers, respectively); 59-30-201, 59-30-202, 59-30-203, 59-30-204, 59-30-205, and 59-30-206 (carbon tax on motor gasoline, on-road diesel, aviation fuel, natural gas, large emitters, and electricity providers, respectively); 59-30-207 (carbon tax exemptions); 59-30-301 (Carbon Emissions Fund); 59-30-302 (Tax Cut Fund); 63N-2-502 (sales tax administrative changes); 72-2-126 (Airport Fund); and Section 25 (effective date).

Technical overview

The carbon tax is levied in Chapter 59-30, which applies the carbon tax to:

- motor gasoline, on-road diesel fuel, and aviation fuel (sections 59-30-201, 59-30-202, and 59-30-203, respectively);

- natural gas (section 59-30-204, but electricity generators can apply for a refund because electricity is taxed in section 59-30-206);

- consumption by “large emitters” (e.g., cement plants, mining operations, refineries) of coal, off-road diesel (a.k.a. dyed diesel), and fuel gas because these are the major categories of direct fossil fuel consumption not covered above (section 59-30-205, note that “large emitters” are certified by DEQ per section 19-1-207 and that amended returns are covered in section 59-30-104); and

- electricity providers, which are taxed based on their system-wide carbon emissions profile, i.e., in-state power plants are not directly subject to the carbon tax but power consumed in Utah is taxed based on the fuel mix of the electric utility (section 59-30-206, certified by DEQ per section 19-1-208, note that amended returns are covered in section 59-30-104).

Industrial users (agriculture, mining, manufacturing, etc., see the definition in 59-30-102) get a phased-in carbon tax rate for the natural gas, electricity, and “large emitters” portions of the tax, starting at 10% of the standard rate in year 1, then 15% in year 2, etc., peaking at 50% of the standard rate in the second decade and beyond. (Note that off-road diesel is only subject to the carbon tax when used in facilities with more than 10,000 tons of CO2 emissions per year, equivalent to about 1 million gallons of diesel.) Exemptions from the carbon tax are in section 59-30-207. More carbon tax details are in the Title, Definitions and Records sections (59-30-101, 59-30-102, and 59-30-103).

Almost all of this carbon tax revenue goes into the Carbon Emissions Fund created in section 59-30-301. (Note that carbon taxes on motor fuels enter the Carbon Emissions Fund indirectly through section 59-12-103, with a small amount remaining in the Highway Fund, and that taxes on aviation fuels are required to go into an Airport Fund per sections 59-30-203 and 72-2-126.)

The Carbon Emissions Fund then directs money to air quality and rural economic development programs, and to the General Fund and the Education Fund to hold them harmless from various tax cuts, as follows:

- $100m to improve local air quality, including $25m to the CARROT program and $75m for a Clean Air Grants program administered by DEQ per section 19-2-401 (this $75m is instead transferred to the Tax Cut Fund if the state meets Clean Air Act standards); and

- $50m to the Governor’s Office of Economic Development — Rural Employment Expansion Program to “use for diversifying the economy in rural counties and communities”.

- eliminating the state sales tax on grocery store food and on commercial and residential use of electricity and heating fuels (section 59-12-103, see also administrative changes in sections 35A-8-308, 35A-8-309, and 63N-2-502);

- extending and expanding the Retirement Tax Credit (section 59-10-1019); and

- creating a 20% match of the federal Earned Income Tax Credit for low-income working families (sections 59-10-1102.1 and 59-10-1113).

The priority order for these transfers is: first backfilling the Education Fund, then backfilling the General Fund, then $25m for CARROT, then $50m for rural economic development, then $75m for the Clean Air Grants program. Any remaining Carbon Emissions Fund revenue goes into a Tax Cut Fund (section 59-30-302) that the legislature can only use “to lower state taxes, especially for low- and middle-income households and for energy-intensive trade-exposed businesses.” Section 25 establishes an effective date of Jan 1, 2022, with the Retirement Tax Credit (section 59-10-1019) and the 20% match of the federal Earned Income Tax Credit for low-income working families (sections 59-10-1102.1 and 59-10-1113) taking effect in the 2022 tax year.

Details on the various sections of the bill

Introductory material (PDF p1-3).

19-1-207 (PDF p3-5). Certification of large emitters for tax purposes.

This section has DEQ certify CO2 emissions from “large emitters”, defined in 59-30-102 as a facility with over 10,000 metric tons of CO2 emissions from coal, dyed diesel fuel, or fuel gas (equal to about 1 million gallons of diesel fuel; note that a 25,000 metric ton threshold is sufficient to require the facility to report to EPA FLIGHT per 40 CFR 98.2) but not including “an electricity provider, a person that provides electricity to an electricity provider to deliver for consumption, or a person that generates electricity”.

To see how the tax on large emitters works, consider a large emitter like a mining or manufacturing company. The carbon tax has already been applied elsewhere to that company’s consumption of motor gasoline, on-road diesel fuel, aviation fuel, and natural gas (per sections 59-30-201, 59-30-202, 59-30-203, and 59-30-204, respectively) and to that company’s consumption of electricity provided by an electricity provider (per section 59-30-206). What that leaves out is the company’s consumption of coal and of petroleum products other than motor gasoline, on-road diesel fuel, and aviation fuel, for example off-road diesel fuel used in a mining operation or fuel gas used in petroleum refining.

The bill has the large emitter report to DEQ the following:

- the number of metric tons of CO2 resulting from consumption in this state of coal, dyed diesel, and fuel gas by the large emitter;

- the number of short tons of each type of coal combusted, the number of gallons of dyed diesel fuel combusted, and the number of thousand cubic feet of fuel gas combusted, plus the number of metric tons of CO2 resulting from each of these categories; and

- any information provided in that large emitter’s EPA FLIGHT report.

The DEQ then checks to make sure that the report matches up with available information and then issues the large facility with a certificate of “the total number of carbon dioxide emissions that the large facility emitted during the previous calendar year”.

19-1-208 (PDF p5-7). Certification of electricity provider.

This section has DEQ certify “electricity providers”, defined in 59-30-102 as “a person in this state that delivers electricity to customers for consumption.”

To see how the tax on electricity providers works, consider an electricity provider like PacifiCorp. (Operating as Rocky Mountain Power, PacifiCorp serves much of the state; there are also electricity providers associated with UAMPS, UMPA, and Deseret G&T.) The bill has the electricity provider report to DEQ the first six items below to allow for DEQ to make the calculations in the remaining points:

- The number of megawatt hours of electricity that the electricity provider delivered to retail customers in this state.

- The number of megawatt hours delivered to retail customers in all states.

- The number of megawatt hours of electricity from “declared resources” that the electricity provider delivered to retail customers in all states.

- The number of megawatt hours of electricity from “undeclared resources” that the electricity provider delivered to retail customers in all states, calculated by subtracting the number in the previous line from the number in the one before that.

- The carbon intensity of each declared resource.

- Information that the electricity provider reports to FERC or to other states.

- DEQ can also calculate, for each provider, the average carbon intensity of the electricity delivered by that provider, using a weighted average of the declared and undeclared resource information in #3, #4, and #5 (using the default value of 1 metric ton of CO2 per megawatt hour to impute the carbon intensity of undeclared resources).

- Finally, DEQ can calculate, for each provider, the number of metric tons of CO2 associated with electricity delivered to Utah customers, by multiplying #1 by #6. DEQ can then issue the electricity provider with a certificate of “the number of metric tons of carbon dioxide emitted to produce electricity that the electricity provider delivered in the state during the previous calendar year.”

19-2-401 (PDF p7-9). Clean air grant program.

This section creates a program to improve local air quality in Utah. The program is administered by DEQ and must consult with the Air Quality Policy Advisory Board and report annually to the state legislature. The program receives up to $75m per year (see section 59-30-301(5)(b)(ii)) but it “may not award a grant under this section to a proposed project that targets an air quality control region that has achieved attainment status with respect to a pollutant that the project proposes to address”, so if the state meets all of its Clean Air Act obligations then this money goes into the Tax Cut Fund created in section 59-30-302.

35A-8-308 (PDF p9-10). Throughput Infrastructure Fund.

35A-8-309 (PDF p10-11). Throughput Infrastructure Fund administered by impact board — Uses — Review by board — Annual report — First project.

These sections make administrative changes regarding sales tax revenue (see section 59-12-103).

59-10-1019 (PDF p11-14). Definitions — Nonrefundable retirement tax credits.

This section extends and expands the Retirement Tax Credit. The RTC currently provides a tax credit of up to $450 per person for those 65 or older who were born before 1953 (i.e., age 65 in 2018). The new section makes two changes: (1) it boosts the RTC from a maximum of $450 per person to a maximum of $650 per person; and (2) it changes the born-before-1953 requirement to born-before-1963. (PS. Note that the RTC has a phase-out for higher-income taxpayers. The phase-out details remain the same—2.5 cents per dollar in income above a certain threshold, e.g., $32,000 for married filing jointly—but boosting the RTC means that more middle-income households will qualify.)

59-10-1102.1 (PDF p14). Apportionment of tax credit.

This section apportions the state match of the federal EITC (see the next section, 59-10-1113) for individuals who are nonresidents or part-year residents.

59-10-1113 (PDF p14-15). Refundable state earned income tax credit — Definitions — Tax credit calculation — Transfers from Carbon Emissions Tax Expendable Revenue Fund.

This section provides a 20% match of the federal Earned Income Tax Credit for low-income working households.

59-12-103 (PDF p15-31). Sales and use tax base — Rates — Effective dates — Use of sales and use tax revenue.

This is a very long section because the existing sales and use tax language is complicated, but there are only a few changes:

- Lines 521-523, PDF p17: Housekeeping changes.

- Lines 536-541, PDF p18: Eliminates the state portion of the sales tax on electricity and heating fuels for commercial and residential use. (The references are to commercial use, subsection 1(c), lines 462-468, PDF p15-16; and residential use, subsection 1(d), lines 469-476, PDF p16.) The current sales tax rate for those goods is 2%.

- Lines 546-549, PDF p18: Eliminates the state portion of the states tax on grocery store food. The current sales tax rate for that is 1.75%.

- Lines 658-673, PDF p 22: Some housekeeping changes, plus language to ensure that the carbon tax backfills the General Fund for the lost sales tax revenue on food (the reference on line 761 is to 59-30-301(5)(b)(i)) and that the backfilled revenue is treated appropriately for determining the state and local share of that revenue.

- Lines 813-945, PDF p26-31: These edits were in HB304S1; they consist of some housekeeping changes and also zeroing out impacts on earmarked transportation and water funds.

- Lines 947-958, PDF p31: Like about half of the states in the USA, Utah has a requirement in the state constitution (article XIII, section 5(6)) that revenue from taxes on motor fuels—notably motor gasoline and on-road diesel—have go into a highway fund that can be used only for road construction and maintenance. Our measure meets this requirement by putting the revenue from the carbon tax on motor fuels into the state highway fund. At the same time, it takes out of the highway fund a roughly equivalent amount of sales tax revenue that is currently being used to subsidize the highway fund. More specifically, “roughly equivalent” means 95%: for every $100 in carbon tax revenue going into the highway fund, $95 in sales tax revenue comes out of the highway fund to be used for air quality improvements, rural economic development, and offsetting tax reductions. This section of the measure takes the 95% out of the highway fund. The net impact on the highway fund will be modest: the large amount of carbon tax revenue going into the highway fund will be mostly offset by this large amount of sales tax revenue coming out of the highway fund. That leaves two smaller impacts that will also mostly offset each other: (1) a modest reduction in highway fund revenue because the carbon tax will reduce motor fuels consumption, thereby reducing the revenue production from the existing motor fuels taxes; and (2) a modest increase in highway fund revenue because only 95% of the carbon tax revenue going into the highway fund is matched with sales tax revenue coming out of the highway fund.

59-30-101 (PDF p31). Title.

59-30-102 (PDF p31-33). Definitions.

Definitions for the carbon tax.

59-30-103 (PDF p33). Records.

Record-keeping for the carbon tax.

59-30-104 (PDF p33-34). Amended return for large emitter or electricity provider.

Amended returns for large emitters (Section 19-1-207) or electricity providers (Section 19-1-208).

59-30-201 (PDF p34-35). Imposition of a carbon emissions tax on motor fuel.

This section imposes the carbon tax on motor gasoline, starting at $12 per metric ton CO2 (10.67 cents per gallon, see EIA). This portion of the carbon tax piggybacks on the existing per-gallon motor gasoline tax: see the Motor and Special Fuel Tax Act, especially 59-13-201(3)(a).

59-30-202 (PDF p35-38). Imposition of carbon emissions tax on special fuel.

This section imposes the carbon tax on diesel fuel intended for highway use (called “special fuel”), starting at $12 per metric ton CO2 (12.19 cents per gallon, see EIA). This portion of the carbon tax piggybacks on the existing per-gallon special fuel tax; see the Motor and Special Fuel Tax Act, especially 59-13-301. Note that subsection (7) references the International Fuel Tax Agreement (IFTA) provision for interstate trucking.

59-30-203 (PDF p38-40). Imposition of carbon emissions tax on aviation fuel.

This section imposes the carbon tax on aviation fuel, starting at $12 per metric ton CO2 (11.48 cents per gallon for jet fuel, see EIA; note that aviation gasoline would more accurately be a tiny bit different, but since jet fuel is over 99% of aviation fuel used in Utah it made sense to just use the jet fuel number for all aviation fuels). This portion of the carbon tax piggybacks on the existing per-gallon tax on aviation fuel. In accordance with federal DOT requirements, the revenues are placed in the Aeronautics Restricted Account, which is the fund for airports; see 59-13-402.

59-30-204 (PDF p40-42). Imposition of carbon emissions tax on natural gas.

This section imposes the carbon tax on natural gas, starting at $12 per metric ton CO2 (63.74 cents per thousand cubic feet, see EIA). The tax is levied on the “purchaser” (“a person in this state that buys natural gas for consumption”) but collected and remitted by the “natural gas supplier” (“a person supplying natural gas to a purchaser”). The tax does not apply to “electricity providers for natural gas purchases that are also subject to a tax under [electricity] Section 59-30-206” (i.e., this portion of the tax doesn’t apply to electricity generators because electricity is taxed based on consumption, not production). Note that industrial use (agriculture, mining, manufacturing, etc., see the definition in 59-30-102) gets a phased-in carbon tax rate for this portion of the tax, starting at 10% of the standard rate in year 1, then 15% in year 2, etc., peaking at 50% of the standard rate in the second decade and beyond.

59-30-205 (PDF p42-44). Imposition of carbon emissions tax on large emitters.

This section imposes the carbon tax on large emitters, starting at $12 per metric ton CO2, for emissions from combustion of coal, dyed diesel fuel, or fuel gas. “Large emitter” is defined in Section 59-30-103 as a facility—excluding power plants, because electricity is taxed based on consumption, not production, per the next section, 59-30-206—that emits a combined total of over 10,000 metric tons of carbon dioxide in a calendar year from combustion of coal, dyed diesel fuel, or fuel gas. See Section 19-1-207 for certification, and note that for dyed diesel fuel, 10,000 metric tons is equivalent to about 1 million gallons of dyed diesel fuel per year. (See EIA, and note that 1 metric ton is 1000 kg.) Also note that industrial use (agriculture, mining, manufacturing, etc., see the definition in 59-30-102) gets a phased-in carbon tax rate for this portion of the tax, starting at 10% of the standard rate in year 1, then 15% in year 2, etc., peaking at 50% of the standard rate in the second decade and beyond.

59-30-206 (PDF p44-46). Imposition of carbon emissions tax on electricity provider.

This section imposes the carbon tax on electricity providers, starting at $12 per metric ton CO2. See Section 19-1-208 for certification. Note that industrial use (agriculture, mining, manufacturing, etc., see the definition in 59-30-102) gets a phased-in carbon tax rate for this portion of the tax, starting at 10% of the standard rate in year 1, then 15% in year 2, etc., peaking at 50% of the standard rate in the second decade and beyond.

59-30-207 (PDF p46). Exemptions.

This section provides a carbon tax exemption for fossil fuels that (a) are brought into the state in the fuel supply tank of a car, etc; (b) the state is prohibited from taxing by state or federal law; or (c) are being exported out of the state.

59-30-301 (PDF p46-48). Carbon Emissions Tax Expendable Revenue Fund.

This section creates the Carbon Emissions Fund. Note that the priority order for spending money in this fund is (per Subsection 6) determined by Subsection 3 to be (a) transfers to the Education Fund to hold it harmless from the revenue reductions resulting from the EITC, Retirement Tax Credit, and ag/mining/manufacturing provisions in this measure; (b) transfers to the General Fund to hold it harmless from the revenue reductions resulting from the elimination of the state sales taxes on grocery store food and on electricity and heating fuels; (c) $25m to the CARROT air quality program; (d) $50m for rural economic development; (e) $75m for the Clean Air Grant program create in Section 19-2-401; and (f) the Tax Cut Fund described in the next section.

59-30-302 (PDF p48). Carbon Emissions Tax Refund Restricted Account (aka Tax Cut Fund).

This section creates a Tax Cut Fund (formally the Tax Refund Restricted Account) in case the carbon tax brings in more revenue than the tax cuts described above. The excess revenues are put in this account, which the legislature can only use “to lower state taxes, especially for low- and middle-income households and for energy-intensive trade-exposed businesses.”

63N-2-502 (PDF p48-52). Definitions.

This section includes only one small housekeeping change: a changed reference (toward the end, in subsection 28) to sales taxes imposed under 59-12-103 because the state sales tax will be zeroed out for grocery store food and for electricity and heating fuels.

72-2-126 (PDF p52-53). Aeronautics Restricted Account.

The only edit here involved putting into this account revenue from the carbon tax on aviation fuels in 59-30-203

Section 25 (PDF p53). Effective date.

Effective date is Jan 1, 2022, with the Retirement Tax Credit (section 59-10-1019) and the 10% match of the federal Earned Income Tax Credit for low-income working families (sections 59-10-1102.1 and 59-10-1113) taking effect in the 2022 tax year.